Tile roof insurance Arizona homeowners rely on covers more than the tiles you can see from the street. Your tiles are intact, no visible damage, but your carrier just flagged the roof on inspection and you’re looking at a 25% surcharge or a non-renewal notice, because what they inspected wasn’t the tile. It was what’s underneath it.

Key Takeaways:

- Concrete roof tiles can last 50+ years, but the felt underlayment beneath them typically fails at 20-30 years, and Arizona’s heat cycle accelerates that degradation.

- Carriers apply a 25-50% age surcharge on homes with underlayment estimated at 20+ years old, per the roof age schedule filed with DIFI, even if every tile on your roof is uncracked.

- An ACV settlement on an aged tile roof can leave you with a five-figure out-of-pocket gap: on a $30,000 re-roof, ACV depreciation of 40-50% means the carrier pays $15,000-$18,000 and you cover the rest.

What Tile Roof Insurance in Arizona Actually Covers, and What Most Homeowners Assume Wrong

Arizona tile roof coverage is the portion of your homeowners policy that pays for sudden and accidental damage to your roof system from a covered peril, storm, hail, wind, falling objects. This means the policy is not a maintenance contract. It does not pay for the underlayment wearing out over time from heat exposure, age, or normal use. That gap is where most Arizona homeowners get surprised.

The standard HO-3 homeowners policy, the form filed and approved by the Arizona Department of Insurance and Financial Institutions (DIFI), covers the roof structure as part of Coverage A (the structure of your home). Per DIFI-filed HO-3 form standards, coverage applies to physical loss caused by a named or open peril depending on policy type. Gradual deterioration, wear and tear, and maintenance-related failures are excluded under standard policy language. The underlayment failing because it is 28 years old is maintenance wear. A storm punching through it is a covered event.

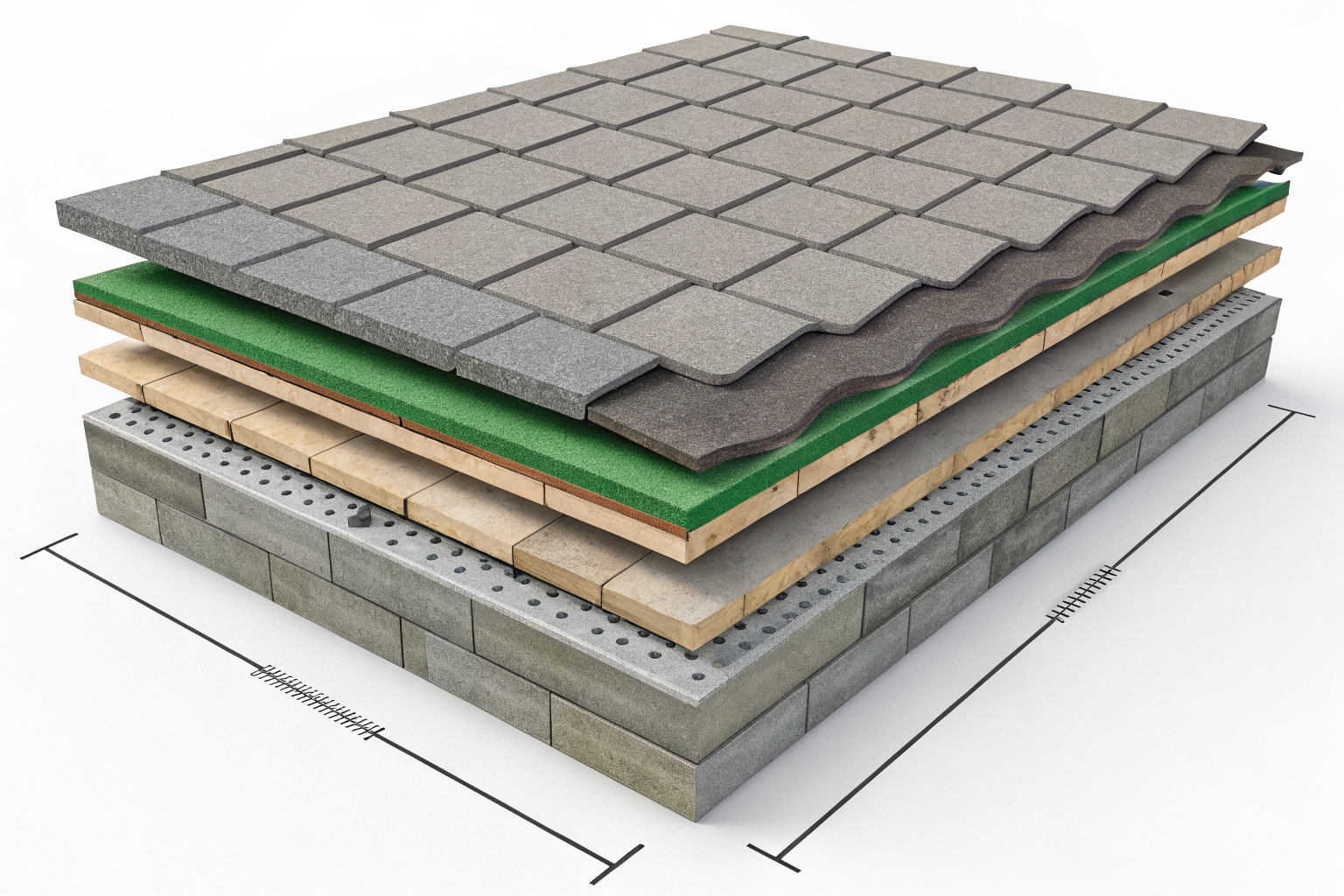

Here is the misconception that costs Arizona homeowners: tile is not the roof. Tile is the surface layer. A concrete or clay tile carries a manufacturer-rated lifespan of 50 years or more. The asphalt felt or synthetic underlayment membrane beneath those tiles is rated for 20-30 years under standard installation conditions, and Arizona’s summer heat compresses that window further. Tiles can look perfect while the waterproofing layer beneath them is at or past the end of its functional life.

From an underwriting standpoint, your carrier does not care how the tiles look. What they care about is whether the waterproofing membrane is still functional, because when it fails, water gets into the structure, and water claims cost money. That is what an inspection is actually measuring.

This distinction matters enormously for anyone navigating the broader arizona insurance guide for homeowners, the tile surface is cosmetic, the underlayment is the insurable component. Readers should consult a licensed Arizona insurance agent for advice specific to their property and policy, as coverage terms vary by carrier and individual policy form.

Why Carriers Look at the Underlayment, Not the Tile, During an Inspection

Underwriting inspection targets the underlayment’s estimated age as the primary insurability signal for Arizona tile roofs. Carriers do not climb up and peel back tiles to inspect the membrane directly on every property. They use a combination of tools to estimate the underlayment’s age and condition: building permit records pulled from county assessor and building department databases, aerial imagery analysis services that capture roof condition over time, and physical inspection when the property warrants a closer look.

Permit records are the backbone. When a re-roof was permitted in Maricopa County, that record exists. Carriers pull it. The permit date tells the underwriter when the underlayment was installed, and from that date, they calculate where the roof sits on their filed age schedule. If no re-roof permit exists and the home is 25 years old, the underwriter assumes the original underlayment is still in place.

Aerial imagery services (the category of vendor that captures geo-referenced overhead photography of properties) give carriers a view of the tile surface condition and can identify cracked or displaced tiles, soft spots, or drainage patterns that suggest underlayment compromise. These services have become standard in AZ homeowners underwriting over the past decade. The tile surface condition from aerial review is one input; the permit-derived age is the controlling factor.

The reason Arizona is particularly punishing on this point is the heat. Arizona attic temperatures reach 140-160°F in summer, per University of Arizona Cooperative Extension research on residential heat exposure. Standard 30-pound felt underlayment is designed for temperature ranges well below that ceiling. At sustained extreme heat, the asphalt in the felt oxidizes, the material becomes brittle, and the waterproofing integrity degrades, faster than the rated lifespan would suggest in a temperate climate. A 20-year-old underlayment in Phoenix has experienced a cumulative heat load that a 20-year-old underlayment in Oregon has not.

Carriers account for this by filing a roof age schedule with DIFI. The schedule defines when surcharges apply, when inspection is required, and when the carrier has the option to non-renew based on estimated underlayment age. Per filed roof age schedule patterns in Arizona HO-3 underwriting, the 25-50% age surcharge typically triggers at an estimated underlayment age of 20+ years. The tile surface condition may influence the size of the surcharge or whether a physical inspection is ordered, but the age trigger is set against the underlayment clock, not the tile clock.

The practical consequence: you can have a tile roof that looks pristine from the street, has no cracked tiles, no storm damage history, and still get a renewal notice with a 25% surcharge attached. Nothing went wrong. The underlayment just got old.

Underlayment Lifespan vs. Tile Lifespan: The Numbers Side by Side

The core problem in tile roof insurance for Arizona homeowners is a mismatch in lifespans. The tile outlives the underlayment by decades. Carriers price that gap into their filed age schedules. The table below makes the comparison direct.

| Component | Manufacturer-Rated Lifespan | Typical AZ Real-World Lifespan (Heat Adjusted) | Carrier Surcharge Trigger Age | Underwriting Action at Threshold |

|---|---|---|---|---|

| Concrete tile | 50+ years | 50+ years | Not a trigger | No action based on tile age alone |

| Clay tile | 50-100 years | 50+ years | Not a trigger | No action based on tile age alone |

| Asphalt felt underlayment (30 lb) | 20-30 years | 15-20 years in AZ conditions | 20+ years estimated age | 25-50% surcharge; inspection required |

| Synthetic underlayment | 25-50 years | 20-30 years in AZ conditions | 25+ years estimated age | Surcharge eligible; carrier-dependent |

Per filed roof age schedule patterns observed in Arizona HO-3 underwriting, non-renewal eligibility typically begins at an estimated underlayment age of 25-30 years, depending on the carrier’s specific filed schedule. Some carriers set a harder line at 25 years; others allow a physical inspection or a licensed contractor certification to extend the underwriting window.

The tile lifespan significantly exceeds the underlayment lifespan, and Arizona carriers price that gap directly into their roof age schedules. A home with original 1995 construction has concrete tiles that could last another 30 years and underlayment that, in Arizona heat, may be approaching or past its functional end. The carrier sees a liability, not a well-maintained roof.

This lifespan gap is also the reason the question of whether a new roof lowers insurance costs matters so concretely for Arizona homeowners: a full re-roof with new underlayment resets the age schedule clock and removes the surcharge trigger entirely.

What Happens to Your Tile Roof Insurance Claim When the Underlayment Is Old?

An ACV settlement on an aged tile roof reduces the claim payout by 40-50% relative to full replacement cost on an Arizona tile roof. Here is how that plays out step by step when you file a claim.

Storm event triggers the claim. A monsoon, hail event, or wind storm causes visible damage to your roof system. You file a claim under your HO-3 policy. The carrier dispatches an adjuster.

The adjuster identifies underlayment age from records. The adjuster pulls the permit history on your property. They note the underlayment installation date, or the original construction date if no re-roof permit exists. The age of the underlayment at the time of loss is now on the file.

Loss settlement basis determines the payout calculation. Actual cash value (depreciated value in consumer language) and replacement cost value (new-for-old) are two different loss settlement structures under standard HO-3 policy language filed with DIFI. If your policy pays ACV on the roof, the carrier applies depreciation against the estimated remaining useful life of the underlayment. If your policy pays RCV, you get the full replacement cost with no depreciation deduction.

On an ACV policy, the depreciation calculation runs against the underlayment. A 25-year-old underlayment with a rated useful life of 20-25 years in Arizona conditions has, from the carrier’s perspective, little to no remaining useful life. Depreciation of 40-50% gets applied to the total re-roof cost.

The homeowner receives a check for the depreciated value, not the re-roof cost. On a $30,000 tile roof replacement, an ACV settlement with 40-50% depreciation applied to aged underlayment yields a carrier payment of $15,000-$18,000, leaving the homeowner with a $12,000-$15,000 out-of-pocket gap.

The ACV versus RCV distinction is the single most important thing to check on your current policy before you have a claim. Your declarations page will list the loss settlement basis. Some policies include a roof payment schedule endorsement (an add-on to the main policy form) that specifies ACV settlement for roofs over a certain age even if the main policy otherwise pays RCV. That endorsement can be easy to miss. Per standard HO-3 policy form language filed with DIFI, the loss settlement basis for the roof structure is controlling, and it may differ from the settlement basis for your personal property or other structures.

If you cannot tell from the declarations page whether you have ACV or RCV on the roof, call your agent and ask directly. The answer to that question determines your real financial exposure before the next monsoon season.

What to Do Before Your Next Renewal If Your Tile Roof Is Over 20 Years Old

An annual disclosure review prevents the ACV settlement gap and the non-renewal surprise for Arizona homeowners with aging tile roofs. Generic advice to “talk to your agent” is not enough here. These are the specific steps that matter.

Pull your permit records before your carrier does. Your county assessor’s office or building department has the permit history on your property. In Maricopa County, permit records are searchable online. The re-roof permit date is the underlayment installation date your carrier will use. Know what that date is before renewal, because if the record shows a 1998 re-roof, you already know how the underwriter is going to read your age schedule position.

Check whether your current policy pays ACV or RCV on the roof. Look at your declarations page for the loss settlement basis. If there is a roof payment schedule endorsement attached to your policy, read it. If your policy is paying ACV on a roof over 20 years old, you are carrying a five-figure gap exposure on every storm claim. That is the conversation to have with your agent at renewal, not after a claim.

Ask your agent what your carrier’s filed roof age schedule says. Carriers file their underwriting criteria with DIFI. Your agent can tell you where your roof’s estimated underlayment age sits relative to your current carrier’s surcharge and non-renewal thresholds. If you are already past the 20-year trigger, you should know whether the next renewal brings an inspection requirement or a surcharge increase.

Ask about a roof certification from a licensed AZ roofing contractor. Arizona requires roofing contractors to hold an active ROC (Registrar of Contractors) license. A licensed contractor’s written assessment of underlayment condition is a recognized document in some carrier underwriting reviews. Some carriers will accept a current certification as an underwriting bridge, evidence that the underlayment, while aged, remains in functional condition. Not every carrier accepts this, but it is worth asking before you spend $30,000 on a re-roof to stay insurable.

Do not wait for a claim to find out your payout basis. The annual review is when you have leverage. At claim time, the policy terms are fixed. Before renewal, you can change them.

If your current carrier’s roof age schedule is working against you and you are facing a surcharge or non-renewal, the market is the answer. With access to 200+ carriers in our network, The Gebhard Agency shops your situation against carriers whose filed age schedules may treat your specific roof age and condition differently. Different carriers have different underwriting appetites for aging tile roofs in Arizona. One carrier’s non-renewal is another carrier’s standard issue, you need someone who knows which is which.

Frequently Asked Questions

Does homeowners insurance cover tile roof underlayment replacement in Arizona?

A standard HO-3 homeowners policy covers sudden and accidental damage to the entire roof system, underlayment included, when a covered peril like wind or hail causes the loss. What it does not cover is gradual underlayment deterioration from age or heat exposure, which carriers and DIFI-filed policy language treat as maintenance wear. If your underlayment has failed without a triggering storm event, that replacement cost is on you.

How do insurance companies know how old my tile roof underlayment is in Arizona?

Carriers use building permit records, aerial imagery analysis services, and physical inspection to estimate underlayment age, independent of how the tiles look from the street. County assessor and building department permit records are the primary data source, and they are the same records your carrier’s underwriting team will pull at renewal. Pulling your own permit history before renewal puts you on equal footing with your carrier’s information.

Will my insurance company pay to replace my whole tile roof after a storm claim in Arizona?

Whether your carrier pays for a full replacement depends on your policy’s loss settlement basis: ACV (depreciated value) or RCV (new-for-old). On an aged tile roof with a 25-year-old underlayment, an ACV settlement applies heavy depreciation to the underlayment layer and can reduce your payout by 40-50% relative to the full re-roof cost. Check your declarations page or any attached roof payment schedule endorsement before you file a claim, not after.