Slow leak vs burst pipe coverage is the dividing line that decides most AZ water damage claims before an adjuster ever sets foot in your home. Your pipe burst at 2 AM and soaked three rooms, that claim pays. Your pipe dripped behind the drywall for six months and rotted the subfloor, that one doesn’t. Same home, same water, completely different outcome.

Key Takeaways:

- Burst pipe claims are covered under most AZ HO-3 policies as sudden and accidental losses, the standard requires the damage to happen within hours or days, not weeks.

- Slow leak claims are denied under the gradual loss exclusion in the standard HO-3 form, filed HO-3 language bars damage that results from continuous or repeated seepage over weeks or months.

- The hidden water damage endorsement (HWDE) is the only add-on that bridges the slow-leak gap, it covers concealed leaks you could not have detected, but it requires documented evidence of concealment to survive a carrier challenge.

The One Line in Your HO-3 Policy That Decides Every Water Claim

The HO-3 gradual loss exclusion eliminates coverage for slow leak water damage claims. That one sentence is the reason so many AZ homeowners get a denial letter after months of damage accumulate inside a wall they never knew was wet.

The sudden-and-accidental standard is the baseline test every water claim must pass on a homeowners insurance HO-3 policy. In plain language, it means the damage had to happen in a single, discrete event with a clear start time, a pipe rupturing at pressure, a supply line snapping under the sink, a water heater tank splitting open. The cause and the damage are connected by hours or, at most, a couple of days.

The gradual loss exclusion sits on the opposite side of that line. It is explicit language in the filed HO-3 form that bars coverage for seepage, leakage, or continuous moisture intrusion that builds over weeks or months. The HOAIC Arizona HO-3 policy form, filed with DIFI in March 2025, uses that exact language, continuous or repeated seepage is excluded, period.

Here is what most homeowners miss: the exclusion applies regardless of whether you knew about the leak. Intent is not the question. Timeline is. A carrier does not need to prove you saw water staining and ignored it. They need to show the damage developed gradually. If their adjuster finds evidence that the moisture was present for weeks before it became visible, the gradual loss exclusion applies, and the claim is denied.

This is also why the hidden water damage endorsement arizona carriers offer exists as a separate, optional add-on. Without it, the base HO-3 leaves slow leaks entirely unprotected. The broader arizona insurance guide covers all six coverage pillars where gaps like this appear, but the burst-vs-leak distinction is the sharpest one most homeowners encounter.

Burst Pipe vs. Slow Leak: Exactly Where the Coverage Line Falls

AZ ranks third nationally in non-weather water damage costs, according to the Insurance Information Institute. The majority of those denials trace to gradual loss exclusion application, not flood. Knowing which side of the line your loss falls on before you file changes everything.

The table below maps the three most common water loss types in Arizona against their coverage status, the trigger for each, and what the hidden water damage endorsement changes.

| Loss Type | HO-3 Coverage Status | What Triggers It | HWDE Changes Outcome? | Typical Result Without HWDE |

|---|---|---|---|---|

| Burst pipe (acute rupture) | Covered | Sudden pressure failure, minutes to hours | No change needed | Pays for structure, contents, mitigation, minus deductible |

| Slow leak inside wall or floor | Excluded | Continuous seepage over weeks or months | Yes, if concealment is documented | Denied under gradual loss exclusion |

| Monsoon wind-driven water through sudden breach | Covered | Single storm event creates opening; water enters acutely | No change needed | Pays for storm-caused damage to structure and contents |

| Seepage through chronic foundation crack | Excluded | Repeated moisture intrusion over time | Unlikely, foundation seepage rarely qualifies as concealed | Denied under gradual loss exclusion |

| Water heater slow drip at base | Excluded | Gradual seal failure over weeks | No, accessible, visible area disqualifies HWDE | Denied; area is accessible, not concealed |

| Supply line failure (acute snap) | Covered | Sudden mechanical failure | No change needed | Pays like a burst pipe claim |

AZ monsoon season context matters here. Wind-driven water that enters through a sudden breach during a monsoon storm, say, a window seal that fails under 60 mph gusts on July 15th, is treated as a sudden and accidental loss. The event has a timestamp. That is the covered side. Seepage through a foundation crack that worsens every monsoon season over two or three years is gradual intrusion, and the exclusion applies regardless of how bad monsoon season gets.

The distinction for hardwood floor water damage insurance claims follows the same logic. A burst pipe that soaks your engineered hardwood overnight is a covered sudden loss. A slow leak under that same floor that warps the boards over months gets the gradual loss exclusion applied to it, unless a hidden water damage endorsement is on the policy and the concealment test is met.

Is a Slow Leak Covered by Insurance, and What Does ‘Due Diligence’ Actually Mean?

When a carrier reviews a slow leak claim, the first question an adjuster asks is not “did the homeowner know?” The real question is “should the homeowner have known?” That is the due-diligence standard, and it is the test that determines whether a slow leak claim survives carrier review.

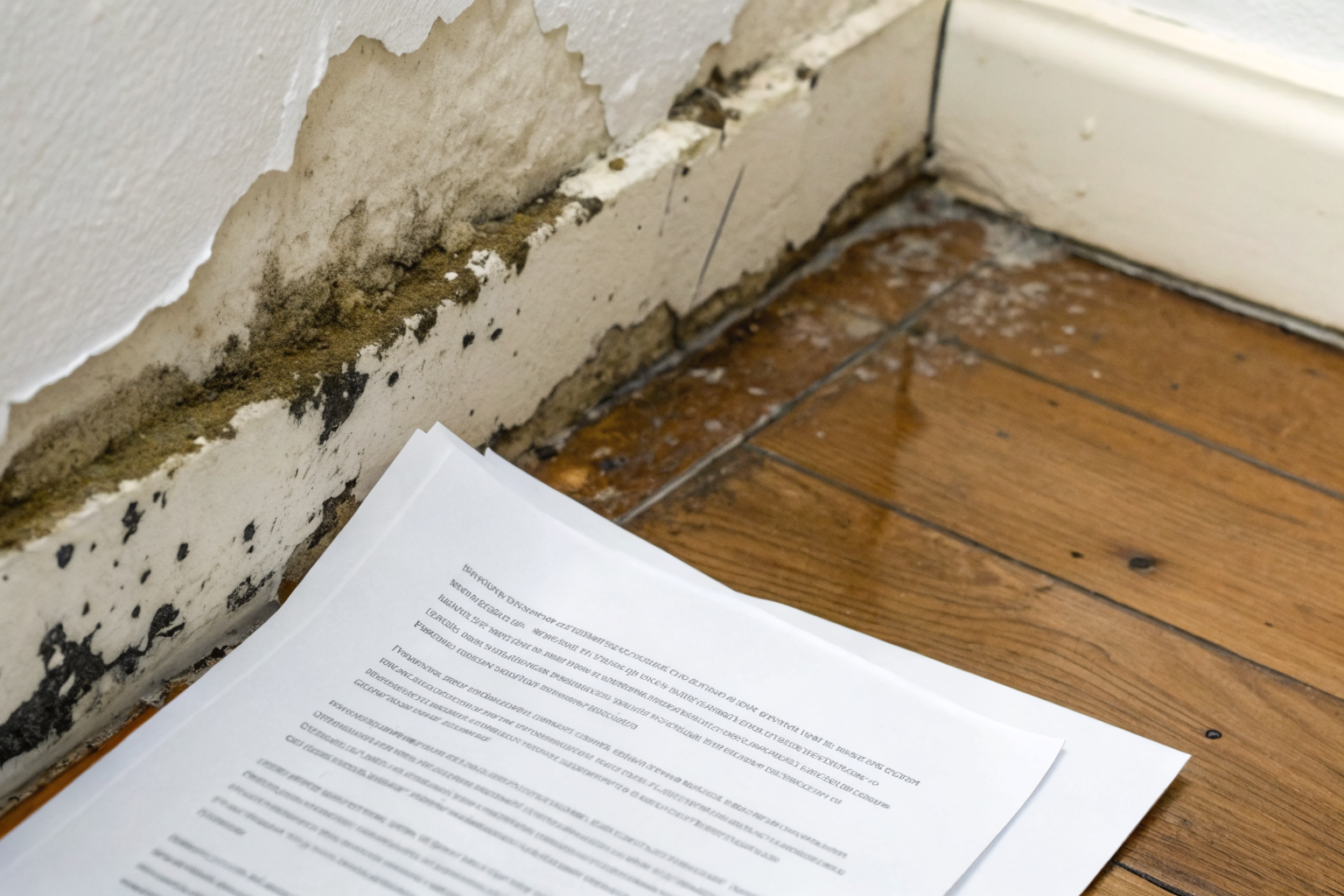

Carriers assess due diligence through physical evidence at the property. Staining patterns on ceilings or walls indicate how long moisture was present before the homeowner found it. Mold growth is one of the most common signals adjusters use, mold visible to the naked eye requires 48 to 72 hours of moisture to develop, so a wall covered in mold tells the carrier the damage was not sudden. Moisture meter readings document current saturation levels, and a skilled adjuster uses those readings alongside the staining pattern to estimate a timeline. Prior maintenance records, or the absence of them, round out the picture.

The argument carriers make is straightforward: if the staining was visible, the homeowner had the information needed to act. Failure to act converts the loss from a sudden event into neglect, and neglect falls outside covered perils.

AZ construction patterns complicate this. Slab foundations in Phoenix metro homes mean there is no crawlspace to inspect. Tile-over-drywall construction in bathrooms and kitchens creates enclosed cavities where a leak can run for months before any surface evidence appears. These are the factual conditions that form the basis for a hidden water damage endorsement claim, the leak was concealed by the structure itself, not ignored by the homeowner.

FNOL claim filing timing matters here too. Reporting the damage on the day you discover it, not two weeks later after mitigation is already underway, establishes the discovery date in writing. Carriers use FNOL date against physical evidence. A late FNOL with extensive mold present creates an obvious gap that adjusters fill with the gradual loss exclusion.

For homeowners who want to understand what counts as hidden damage signs before a claim ever happens, the practical answer is: look inside enclosed cavities during any remodel or repair, and document what you find.

What the Hidden Water Damage Endorsement Actually Does, and When It Pays

The hidden water damage endorsement closes the coverage gap for slow leaks that could not have been detected before they caused damage. It carves a defined exception into the gradual loss exclusion for concealed leaks inside walls, floors, or ceilings that were not visible or accessible. Without it, those losses are simply uninsured on a base HO-3.

Here is how it works in practice:

Request the endorsement at renewal by name. Ask your agent for the hidden water damage endorsement specifically. It does not appear on a base HO-3 quote, and carriers do not offer it proactively. The underwriting question will typically ask whether the home has had prior water damage claims or known plumbing issues.

Understand the concealment test before you need it. The endorsement covers leaks that were inside an enclosed cavity, behind drywall, under a concrete slab, inside a ceiling cavity, and were not visible or accessible without opening a wall or floor. A leak under a sink does not qualify because that space is accessible. A supply line running inside a finished wall does qualify.

Document concealment before mitigation begins. Before any contractor opens the wall, photograph the undisturbed surface from every angle. Timestamped photos showing no visible staining on the exterior surface are the primary evidence that the leak was hidden. Once remediation is underway, that evidence is gone.

Know the sub-limit before you rely on it. HWDE sub-limits on standard AZ endorsements run $5,000 to $10,000. Full water remediation in a Phoenix metro home, including drywall removal, drying, mold treatment, and reconstruction, runs well above that range based on contractor reports. The endorsement is a meaningful gap-closer, but it is not a full remediation policy.

File FNOL the day you find it. The discovery date you establish at FNOL is the anchor for the concealment argument. If you wait two weeks, the adjuster’s timeline reconstruction using mold patterns and moisture readings may contradict it.

One practical note for homeowners who review policies at renewal: if your carrier raised your deductible at renewal without flagging it, the HWDE sub-limit conversation becomes even more important. A $10,000 endorsement sub-limit against a $15,000 deductible leaves you exposed. That mismatch is worth reviewing before the next monsoon season.

What Evidence Does an Adjuster Actually Want for a Water Damage Claim in AZ?

Evidence requirements determine whether a water damage claim survives or gets denied under AZ HO-3 review. The adjuster arriving at your home is not just assessing damage, they are building a timeline. Your job is to make that timeline support your claim, not undermine it.

Here is what an AZ adjuster looks for when assessing a claim at the burst-vs-leak boundary:

Timestamped photos taken before any mitigation work begins. Photograph the damage location, the access point, and the surrounding undisturbed surfaces from multiple angles before a contractor touches anything. These photos establish the condition at discovery, which is the starting point for the adjuster’s assessment.

A written plumber’s report identifying the cause, location, and nature of the failure. The report should state whether the failure was acute (sudden pressure rupture, fitting snap) or chronic (gradual corrosion, slow seal degradation). An adjuster gives a plumber’s written finding significant weight against the gradual loss exclusion.

Moisture meter readings from a licensed contractor, not just visual inspection. Visual inspection tells an adjuster what is wet now. Meter readings document the saturation pattern and depth, which helps establish whether the moisture spread from a single point event or accumulated over time from multiple directions.

Prior maintenance records, or documented absence of them. If you have records showing the plumbing system was recently inspected and no issues were found, that directly supports the sudden-loss argument. No repair history is also useful: it shows you were not ignoring a known problem.

The date of first discovery, documented in writing at FNOL. Do not reconstruct the discovery date from memory in a later conversation with the adjuster. State it in the initial FNOL filing. If you found water on a Tuesday evening, that date goes into the FNOL on Tuesday evening.

For HWDE claims specifically: evidence that the leak location was physically enclosed and not accessible without opening a wall or ceiling. Photos of the undisturbed wall surface before demolition, combined with the plumber’s report identifying the leak location inside the cavity, are the two documents that carry an HWDE claim through a carrier challenge.

AZ monsoon season runs from July through September, and adjusters handling high claim volume during that period issue initial denials under the gradual loss exclusion at a higher rate. Having this evidence package ready at FNOL reduces the back-and-forth rounds that slow claim resolution. Carriers report that incomplete first reports are the primary cause of claim cycle delays, not disputed coverage positions.

Homeowners in areas where HOA master policies create coverage ambiguity, a pattern common in Gilbert canal-adjacent communities and Scottsdale high-rise condos, should also clarify whether the water source originated inside or outside the unit boundary before filing. That distinction affects which policy responds first and how evidence requirements shift.

Frequently Asked Questions

Does homeowners insurance cover a slow leak under the sink?

A slow leak under the sink is excluded under the gradual loss exclusion in a standard AZ HO-3 policy because the damage developed over time in an area that was visible and accessible. The hidden water damage endorsement does not apply in this situation, the space under a sink is open and reachable, so the concealment test fails. The best outcome is a partial pay if the drain fitting snapped abruptly and caused a sudden overflow, but a chronic drip gets denied.

What does a burst pipe insurance claim cover in Arizona?

A burst pipe claim on an AZ HO-3 policy covers the resulting water damage to structure and personal property, drywall, flooring, cabinetry, and contents, but not the cost to repair or replace the pipe itself. The pipe is part of the home’s mechanical system, not a covered peril. Mitigation costs including water extraction and drying are covered under most policies, subject to your deductible.

Can I add water damage coverage for slow leaks to my existing Arizona homeowners policy?

Yes. The hidden water damage endorsement is the add-on that extends coverage to concealed slow leaks inside walls, floors, or ceilings that were not discoverable before damage occurred. Not every AZ carrier offers it, and those that do apply a sub-limit that typically runs $5,000 to $10,000. Ask for it by name at your next renewal, it does not appear on a standard HO-3 quote without a specific request.